1.Introduction.

ESG finance is a topic that challenges all components of the financial system and the corporate world more generally. However, is it a transitory or structural phenomenon? And what is its real impact on corporate behavior? The starting point for any answer must be an understanding of what is at stake. If we look at the world’s financial resources, the liquidity available today — and therefore immediately investible — amounts to 110 trillion euros, an amount higher than the world’s GDP, which is 90 trillion.

Total financial wealth amounts to almost 300 trillion and if we look at a country like Italy , that in the hands of households is now 4.8 trillion euros, or three times Italy’s GDP, and a third of this wealth is liquid. How these resources are invested can make a real difference. Hence the unrepeatable opportunity for many companies to open up their capital and intercept these resources that can change their size and destiny, but also the development of investments that are increasingly directed towards illiquid assets, such as real estate, private equity and venture capital. The multiplication of financial instruments creates an increasingly important and articulated bridge between savings and the ESG finance is at this juncture, with the double face of both a new investment product and a different modality and therefore transversal to any financial instrument, from liquid equity to real estate. The sector today encompasses and surpasses many experiments that have characterized the market over the last thirty years: forms of “social” finance rather than CSR-related instruments have occupied the market in a worthy but marginal way, based on a very simple idea of “discount”: the investor renounces a large part of his return, reaping the moral benefit of having contributed to a just cause.

The ESG perspective is radically different, asking not the saver to make a sacrifice, but the financed subject to adopt active and effective policies and behaviors for their impact along the environmental (E), social (S) and corporate governance (G) dimensions. This is not only to generate a “moral” benefit for the community but also a substantial one, capable of reconciling the dimension of production and jobs growth with that of the wider social return.

This is possible thanks to the awareness that certain trends can seriously and definitively compromise our eco-system and the ability of companies themselves to produce: water scarcity, the use of fossil fuels, air and water pollution, and to support and operationalize these choices, assuming the role of a structural and definitive phenomenon. The social dimension is therefore no longer a discount, but rather a premium as it creates room for growth, compatible with the protection of our eco-system.

The EU Taxonomy for Sustainable Activities.

| Environmental | Social | Governance |

|

|

|

- “E” stands for environmental strategy assessment, policy, and management system, and the industry-specific environmental impact of production.

- “S” stands for strategy and social policy, which assesses the quality of the company’s relations with its stakeholders (customers, competitors, employees, management, public and regulatory bodies, shareholders, creditors, local government, international institutions), market positioning, and competitor analysis; and

- “G” stands for governance structure and assesses both market and internal management issues, identifies the company’s governing bodies structure and main operational characteristics, and connects it with the political, regulatory, and legal specificities of the company’s jurisdiction.

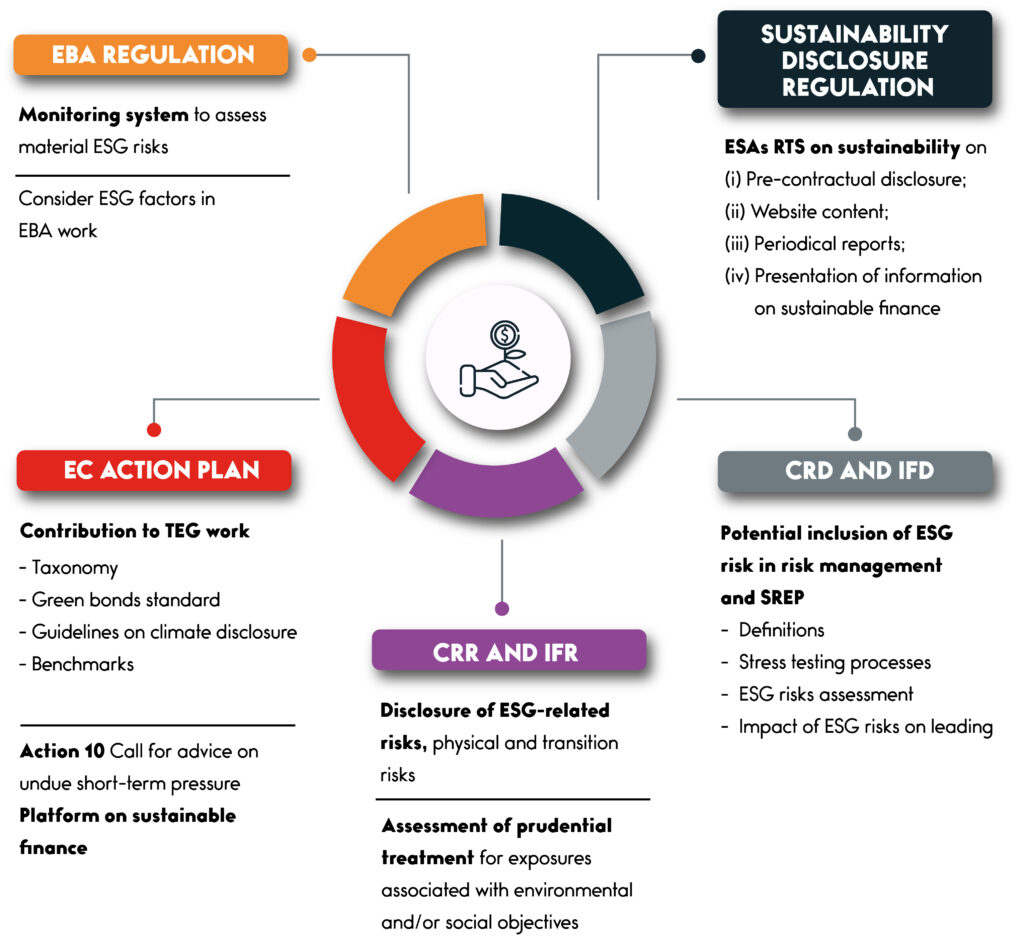

3. Market composition.

If we look at the composition of the market, it develops along the two different lines of action of bonds and equity. In the first case, the most widespread bonds are green bonds, followed by social and then sustainability bonds for a total of 500 billion euro of which 31 in Italy. Afme’s Capital Market Union report indicates that in the EU, bonds qualifying as EGMs now amount to 16% of total issues, while the figure remains surprisingly low in the US market, at less than 1% of issues.

and bans on activities that the company cannot do, to a more proactive stance of stimulating wide-ranging interventions that must be defined, implemented and measured in their effects by the companies. The European Union has laid down the definitions and main metrics for measuring the ESG dimension for companies in the EU Sfdr — Sustainable Finance Disclosure Regulation, and the resources involved are increasingly significant: to date, 7,486 funds worldwide (of which 6,147 in Europe) qualify as ESG instruments, with a growth of EUR 185 billion by 2021. The availability of ratings is therefore becoming essential, and while their proliferation is understandable, it may nevertheless generate distortions in the allocation of resources.

According to Wbcsd (World Business Council for Sustainable Development) data, at the end of 2020 there is evidence of 40 ratings, 150 rankings and 450 EGD indices on the market. Many of these have a very low correlation with each other, indicating that there is still a long way to go to achieve an unambiguous and adequate reading. It is no coincidence that, in 2021, Esma sent a letter to the European Commission with a view to setting adequate standards on the subject of ESG ratings, so as to avoid both greenwashing and displacing entire areas of companies not represented by the ratings and indicators available on the market resources. The risk is real and will have to be managed, but it is the inevitable step that this profound transformation of both the investment side and the business side entails.

4. Future expectations.

What can we expect in the future? So if the ESG dimension cannot be called transitional, going back to the original question, what will be the impact of sustainable finance?

- Here we can take a position because the impact will be strong and decisive. The first reason is because the cost to companies and states of not adhering to ESG principles is becoming higher and higher. It is not farfetched to imagine that in the short term companies without an EGS rating or with very low values will be cut off from the map of financing and investment. And it is not impossible — and above all desirable! — that this will also happen to states.

- The second is the loss of opportunities: a decisive move towards the ESG dimension for a company means benefiting from higher multiples (because more capital is going in that direction), higher EBITDA (gross margin) growth thanks to ecological or energy transition processes, and a lower cos.

- The third is a demographic fact: by 2029, two-thirds of investors will be millennials and Z-gen. It is more than a hope to bet on a different attitude to the meaning of one’s investment choices and the acceptance of principles that place the eco-system at the heart of decisions.

The power and fascination of this new challenge will be that of being able to write in the history books not so much that a different and ‘better’ finance will have changed the world, but that finance — which, let us remember, needs risk and real returns to create GDP and employment, and to pay for our welfare — will have been decisive in changing the face of our society for the better. How we invest can make a difference.

5.The use of disruptive technology to boost Green Finance.

innovation companies and multinational enterprises are also moving items of value across blockchain networks. The process of tokenization— that is, converting the rights to an asset into a digital token within a blockchain, with one token representing an intangible asset or a defined portion thereof — plays a considerable role in the exchange of information. Everything is recorded on the distributed and decentralized ledger, which increases trust and transparency between counterparts. Lifting responsibilities from the companies that have bee ecosystem to focus on its respective businesses and obligations. They can alsoanticipate their future objectives and projects by using smart contracts.

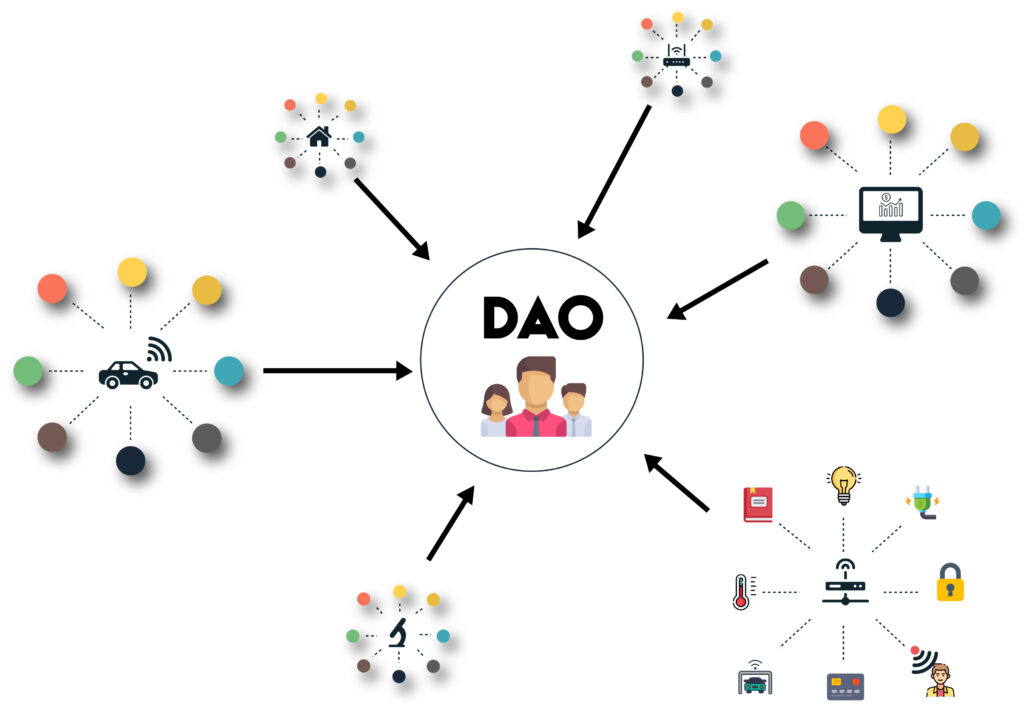

6. DAO — Decentralized Autonomous Organizations.

A DAO is “a community-led entity with no central authority where smart contracts lay the foundational rules and execute the agreed upon decisions.”

Can you imagine a way of organizing with other people around the world, without knowing each other and establishing your own rules, and making your own decisions autonomously all encoded on a Blockchain? Well, DAOs are making this real. DAOs are essentially decentralized communities, where members are incentivized to collaborate with one another to drive value. A DAO’s financial transactions and rules are recorded on a blockchain. This eliminates the need to involve a third party in a financial transaction, simplifying those transactions through smart contracts. The firmness of a DAO is a smart contract. The smart contract represents the rules of the organization and holds the Organization’s storage. No one can edit the rules without people noticing, because DAOs are transparent and public.

In comparison to traditional companies, DAOs have a democratized organization. All the members of a DAO need to vote for any changes to be implemented, instead of implemented changes by a sole party (depending on the company’s structure). The funding of DAOs is mainly based on crowdfunding global, meanwhile, traditional companies’ operations are private, only the organization know what is happening, and they are not always global.

7. Conclusions.

The twin Green and Digital Transformation is a key priority for Europe! To realise this green potential, digital technologies need investment and legislation that encourages them to flourish. Europe therefore needs to step up its digitalisation efforts — such as boosting connectivity and increasing funding for research and development. For this to happen, Europe must look at digital and climate action together, rather than separate policy areas. The Next Generation EU, for example, evoking the ambition to lay the foundations for the Europe of the next generation, supported by DIGITALEUROPE whose vision is for Europe to embrace digital in climate action, to bring benefits in the to society at large and to continue its global leadership by collaborating with our international partners.

A greener economy means growth and job opportunities. Eco-design, ecoinnovation, waste prevention, and reusing raw materials can bring net savings of greenhouse gas emissions, according to the European Commission. However, the commission’s statement on the Green Deal suggests it is also politically motivated.

The European Commission has adopted a number of measures to increase sustainable finance. First, the new sustainable finance strategy sets out several initiatives to tackle climate change and other environmental challenges while increasing investment — and the inclusion of SMEs — in the EU’s transition toward a sustainable economy. The European green bond standard proposal, for example, will create a highquality voluntary standard for bonds financing sustainable investment. Finally, the commission recently adopted a delegated act on information to be disclosed by financial and nonfinancial companies on their sustainable activities, based on article 8 of the EU Taxonomy. These initiatives highlight the EU’s global leadership in setting international standards for sustainable finance. The European Commission intends to work closely with all international partners, including through the International Platform on Sustainable Finance, to build a robust international sustainable finance system.

A new Circular Economy Package has been adopted by the European

- Sustainable Products Initiative, including the proposal for the Ecodesign for Sustainable Products Regulation — find out more

https://lnkd.in/dk58nKnM - EU strategy for sustainable and circular textiles — find out more

https://lnkd.in/dk58nKnM - Proposal for a revised Construction products Regulation — find out more

https://lnkd.in/dZgzdYBd - Proposal for empowering consumers in the green transition — find out more

Businesses run on information. The faster it’s received and the more accurate it is, the better. Blockchain is an ideal information tool because it provides immediate, shared, and completely transparent information stored on an immutable ledger that only permissioned network members can access. A blockchain network can track orders, payments, accounts, production processes, and much more. And because members share a single view of the truth, they can see all details of a transaction end to end, giving them increased confidence and opening up new efficiencies and opportunities. This, together with some other feautures, creates a new digital ecosystem in which green finance can flourish.

Author’s Bio

Antonio Lanotte

Mr. Antonio Lanotte is a Chartered Tax Adviser and Senior Auditor, International Tax Advisor. Particularly keen on Digital Transformation (Blockchain, IoT, AI, machine learning) and Circular Economy (Green Tech) with important contributions to international and national press, such as Bloomberg Tax; IBFD-European Taxation; ITR -International Tax Review; TNI - Tax Notes International; IFRL - International Financial Law Review; FinTech Review, Sole 24 ore; Wall Street Italia; and Bollettino Tributario. Results-driven finance, controlling and international taxation with years of experience in industries and consulting in Italy and abroad. He is a member of the Board of Advisors of Vernewell Management Consultancies and a Lecturer at Vernewell Academy, and since October 2019, he has been an active Member/Delegate of the Tax Technology Committee - CFE Bruxelles; Member/Delegate of the Advisory Council of Blockchain for Europe. He is a member of the "Panel of Experts" of the EU Blockchain Observatory & Forum. Actively participates as a "Business Mentor" in technology startup project analysis sessions at the Startup Bootcamp. Last but not least, he contributed to the "Climate Bank Roadmap 2021-2025," financed by the European Investment Bank - EIB.

- [email protected]

- +971 4 584 7767